Boris Johnson, the part-time Cookie Monster and full-time Apprentice, had promised his compatriots a new age of independence following the Brexit, a renewed sense of national pride and prosperity for all. The great Britain would be free from the shackles of Europe. Well, the Brexit has come and gone, and the UK are becoming more and more European. This is becoming visible on many fronts, not least when looking at the development of government bond yields.

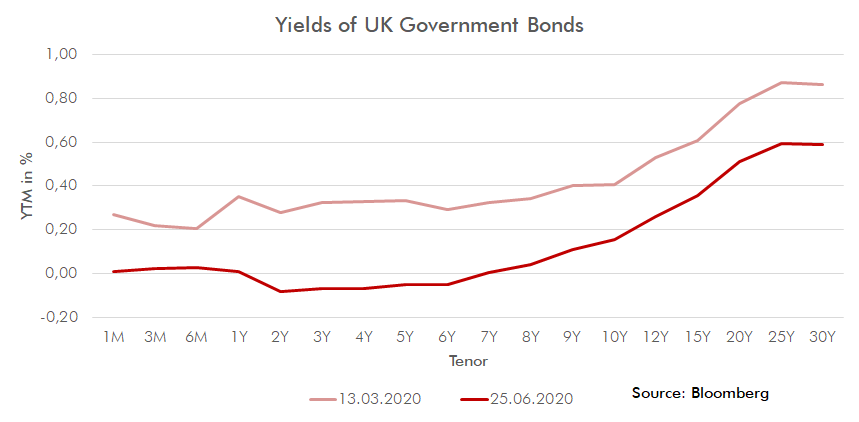

While government bond yields in the USA, the former colony with which the Apprentice was eager to be negotiating at eye-level, are still positive across the curve, UK gilts have just been marking new record lows over two, three, four and five years (and six and seven and eight and nine and ten). Half the curve is now submerged in negative territory, showing a striking resemblance to most curves in the rest of Europe, overall.

Johnson had promised his fellow Britons the quick establishment of free-trade agreements with all of its most important trading partners. After all, who would not want to be in tune with “Global Britain”? Also on the long list of promises were solid finances, a contrast to the profligate Europeans. To top it off, the strong conviction in its own independence was highlighted also symbolically by pursuing a rather solitary path for dealing with the oncoming COVID-19 pandemic. Oh, how it all backfired!

The pandemic has been raging harder though the UK than anywhere else in Europe, reaching almost American proportions. In fact, the speed of the spread was so vicious that it had taken no more than a couple of weeks, before the country had to join in with the same restrictive measures applied throughout most of Europe.

Free Trade Agreements with the most important trading partners? None, so far. Even the old Commonwealth friends could not be persuaded to step in at short-notice for a show of confidence. A couple of agreements with the old EFTA partners, and negotiations with important trading partners that are only now starting, are all there is to show for. International trade is still relying on the EU transition period ending on 31 December 2020. So far, the Apprentice vows that there will be no extension beyond that date. The official deadline to register an extension expires on 1 July. This deadline will pass. However, reality will force its way. Realpolitik will prevail. Given that most of the necessary trade agreements are unlikely to be finalized by year’s end, there is a strong likelihood of a transition period extension past December. At the same time, the UK has no more representation or votes at the EU’s table. Independence, indeed.

Government finances seem to be running amok. The pandemic-induced debt binge is a welcome opportunity to cover-up the economic weakness and loss of jobs that had already started before the pandemic as a result of the Brexit. If the country were a boxer, it would look groggy.

While still a member of the EU, British leaders had always been very vocal when it came to criticizing budgetary policies of some less fortunate Eurozone countries. Now, the United Kingdom stands alone: While government debt is rising to record levels, the Bank of England is forced to keep buying government bonds at unheard of levels, in order to keep interest rates depressed. On average, since late March the BoE has been buying government bonds to the tune of around GBP 13.5 bn per week. This was sufficient to push yields into negative territory and allow the government to issue record amounts of new debt. How euroic!

Goodbye, solid budgets, and goodbye European solidarity.

Bond yields, free trade, budget deficits, debt, public policies …? Instead of becoming independent and powerful, our friends on the other side of the English Channel, realistically speaking, are looking more European than they probably ever have.